Re: Your filing cabinet?

Posted: Sat Nov 18, 2023 10:37 pm

You might be thinking about traditional pensions. A lot of typical pensions for police, fire, teachers, etc. are based on a formula where they take your highest 3 years earnings (or highest 5 years earnings) and multiply that by the number of years that you worked in that profession and then a percentage multiplier.

They look at the average of your 10 highest-earning years across your entire life.

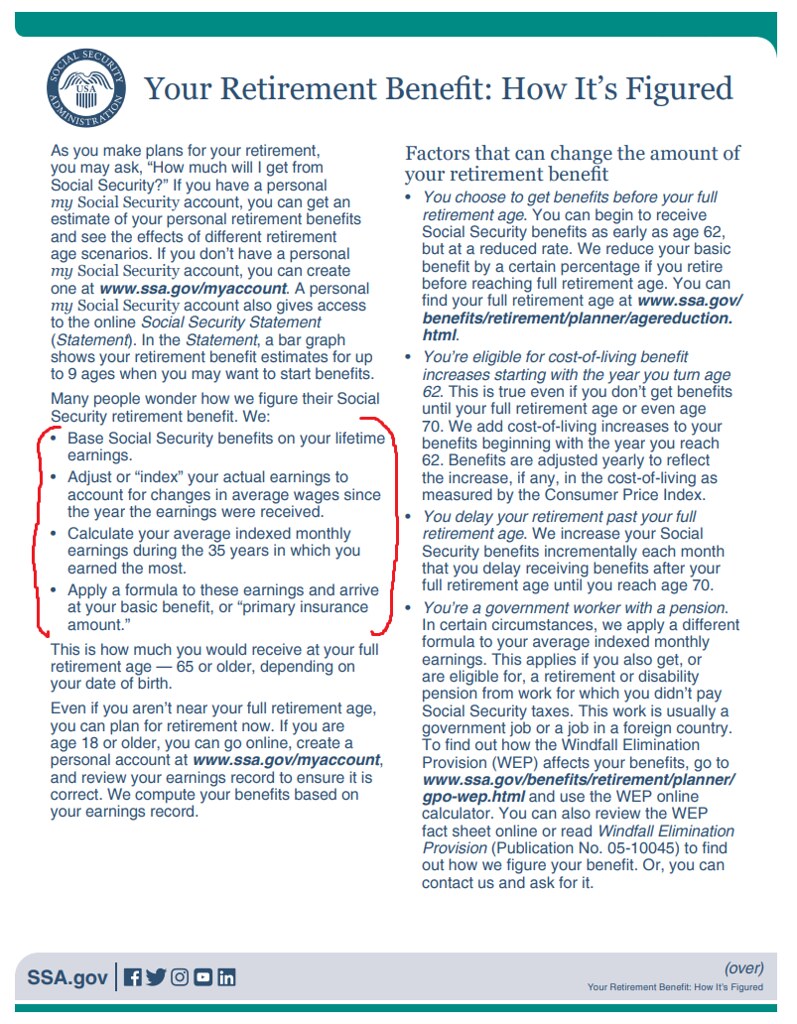

You were misinformed. This information is easy to find. Social Security has all kinds of explainers looking at different scenarios on their web site. Everyone who is going to be eligible for and receive Social Security in their retirement should understand how the program works so they can understand how the choices they make will affect their benefit. Here is Social Security's explainer pamphlet which summarizes it (but they have much more detailed information on their web site): https://www.ssa.gov/pubs/EN-05-10070.pdfJosh wrote: ↑Sun Nov 19, 2023 7:50 amThey look at the average of your 10 highest-earning years across your entire life.

For a typical person these will be their most recent 10 years, due to inflation and the fact people often get raises.

(Or so it was explained to me when I went into the SSA office to fix some identification problems with my account.)

This (the bolded and underlined) is the crux of the matter in our case. By zeroing out the 18 years we were working in Brazil, they reduce my total years to less than 35. I would add that this 35 years of "paying in" is said by many to be a basic requirement. But I have heard all sorts of different explanations and formulas for how the IRS figures a person's SS benefits upon retirement. Not just any average person on the street, or even accountants. There's a radio program on the Moody Radio station here in our area, and they have a bit different understanding of it. Some say it's figured on the last ten years of employment. Others say that it is based on the 10 highest years out of the required 35 years. Etc.Ken wrote: ↑Sun Nov 19, 2023 12:31 pmYou were misinformed. This information is easy to find. Social Security has all kinds of explainers looking at different scenarios on their web site. Everyone who is going to be eligible for and receive Social Security in their retirement should understand how the program works so they can understand how the choices they make will affect their benefit. Here is Social Security's explainer pamphlet which summarizes it (but they have much more detailed information on their web site): https://www.ssa.gov/pubs/EN-05-10070.pdfJosh wrote: ↑Sun Nov 19, 2023 7:50 amThey look at the average of your 10 highest-earning years across your entire life.

For a typical person these will be their most recent 10 years, due to inflation and the fact people often get raises.

(Or so it was explained to me when I went into the SSA office to fix some identification problems with my account.)

So in effect, if you have less than 35 years of employment history when you retire, the formula gives you zeros for all those years up to 35 that you have no Social Security earnings.

There is also the issue of bend-points. https://www.ssa.gov/oact/cola/piaformula.html which are important for people close to retirement age to determine how much continuing to work versus retiring will affect their Social Security payment. Basically if your earnings history is low then you get more credit for future earnings than if it is high. The formula is progressive.

Do your own research if you are eligible for and counting on getting Social Security. There are also various free and paid calculators out there that will let you input your own earnings history and game out different retirement scenarios to figure out how to maximize your benefit. The program is complex.

(The dollar figure always reflects my income from the previous year.)These personalized estimates are based on your earnings to date and assume you continue to earn $---- per year until you start your benefits.